We are living in a moment in history where the Russia-Ukraine war has revealed the weaknesses of European supply chains. The over-reliance of Europe on Russian gas and market reaction saw prices peak 14 times higher than the relative stability of prior years. The subsequent global rerouting of gas supply chains has resulted in the UK importing 50% more LNG than two years ago at increased cost and emissions intensity.

This historic event has brought to light the volatility of a market so reliant on one supply route, in turn highlighting concerns and questions regarding the UK’s energy security. The IEA defines energy strategy as ‘the uninterrupted availability of energy sources at an affordable price’1. Electrification and hydrogen from electrolysis has the potential to redefine global geopolitics as countries move away from being reliant on oil and gas producing nations and provide their own energy.

This would enable many countries to become more self-sustaining and protect against disruptions and price volatility. Countries with higher renewable energy potential will find that ambition more achievable than those without who will likely have to continue to rely on international trade.

To understand the impact hydrogen could have to the UK’s (or indeed any other country’s) energy security, it is important to recognise industries for which hydrogen is a viable option. The media has often presented hydrogen in two opposing spectrums:

- ‘Hydrogen is the silver bullet’ stance

- ‘Hydrogen has limited, to no place, in the future energy mix’

The most commonly cited use case for hydrogen is seemingly road transport, though only two hydrogen cars are currently commercially available, the Hyundai Nexo and Toyota Mirai. Battery-electric vehicles are expected to dominate the passenger car sector in future due to their increasing capabilities and decreasing costs as well as improving levels of charging infrastructure.

Hydrogen cars may see some limited uptake in geographies where distances are very large, but this is not expected to be the case in the UK. The use of hydrogen for domestic and commercial heat is the subject of significant debate. To its supporters, it is a way to decarbonise around a quarter of the UK’s energy use with little change or capital expenditure to the consumer, while reusing existing infrastructure.

To its detractors, it is an inefficient use of energy, consuming six times energy than heat pumps, and will require far more renewable generation to be installed and will have a much higher total cost of ownership. In the UK, the government’s decision on hydrogen for heat has been delayed until 2026, though the recent report from the UK’s National Infrastructure Committee calls on the government to rule out hydrogen for heating2.

For high temperature industrial heat, such as glass or brick manufacturing, hydrogen is likely to be the decarbonisation solution. Large scale uptake is unlikely in the near-term. For mid-temperature heat, such as food production or breweries, the use of hydrogen or high-temperature heat pumps will be made on a case-by-case basis.

Hydrogen is expected to have a place within the decarbonising aviation sector, similarly the maritime sector but via ammonia or e-fuels rather than liquid or gaseous hydrogen predicted for aerospace. Widescale roll out of such solutions are not expected in the near term for aviation and maritime, both due to the lack of cost effectiveness in lower margin sectors and the technology readiness levels (TRLS) of the associated technologies.

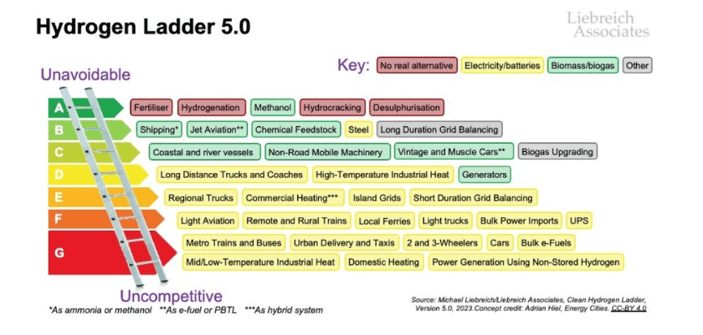

Michael Liebreich, Chairman and CEO of Liebreich Associates created the somewhat infamous ‘hydrogen ladder’ that ranks hydrogen use cases from unavoidable to uncompetitive. Liebreich’s ladder suggests that hydrogen will be a key solution for long duration grid balancing (formerly worded as long-term storage), unsurprising given that such applications would enable higher grid resilience by providing back up power when sectors become more electrified.

The Royal Society’s recent report3 indeed identified that hydrogen can be stored at scale in salt caverns, and although not widely distributed in the UK, there is more than adequate future potential.

This will in various ways contribute to the UK’s energy security, though this will require extensive technology and production scale up. The most recent update in October 2023 saw ‘Power Generation Using Non-Stored Hydrogen’ ranked as one of the most unpractical use cases. In the UK context, this mainly pertains to the ongoing lobbying for hydrogen blending into the gas transmission or distribution grid.

The strategy believes that the UK will utilise its own renewable energy resources, particularly offshore wind, to supply its own energy needs

Hydrogen is touted by many governments as a solution to improve energy security and in the UK, the implementation target for 2030 doubled in the UK Energy Security Strategy

The strategy believes that the UK will utilise its own renewable energy resources, particularly offshore wind, to supply its own energy needs. What’s more, is that UK could become energy exporters, supplying gas to Europe. This is an easy ambition to get behind, but whether it is realistically achievable is harder to navigate.

The UK Government Hydrogen Investor Roadmap shows that the demand by 2035 is expected to be between 55TWh and 165TWh, which equates to 1.6 million tonnes and five million tonnes respectively. For comparison, 1.6 million tonnes is the stated full capacity output of the Australian mega project majority owned by bp.

The ‘Asian Renewable Energy Hub’ project will require 26GW of renewable energy that will take up a land area three times the size of London or half the land area of Northern Ireland. This is almost equivalent to the entire onshore wind and solar capacity we have in the UK today and goes to show the extent of the challenge to produce the lower boundary case for green hydrogen production in the UK.

Offshore wind provides the best option for the industry but provides a challenge in itself as the potential for offshore wind is limited in growth by the availability of wind leasing rounds as well as the lead time to develop projects once won is several years to a decade.

If the UK wants to create enough offshore wind to produce large quantities of domestic green hydrogen, then that needs to be the explicit strategy and the whole sector needs to be pushed forward to achieve those goals; as it stands, the goals are ill-defined.

The alternative is blue hydrogen, which is difficult to count as a ‘solution’ in a 2050 Net Zero world. The price volatility from this global commodity market and decreasing domestic production are a threat to the principles of energy security that hydrogen is meant to bastion.

Furthermore, the extraction of natural gas and methane leakages can be reduced, but never eliminated. The UK’s Low-Carbon Hydrogen Standard will always allow for some level of uncaptured flue emissions. Carbon negative technologies are not yet a feasible solution to be betting on given that biomass derived carbon dioxide is limited in availability and that Direct Air Capture is costly, inefficient, and requires large infrastructure for little capture.

However, the technologies will need to play their role if the UK cannot abate the ‘unavoidable’ carbon emissions. A recently completed study by Ricardo for the Scottish Government found that the maximum potential achievable negative emissions by 2030 fall short and are 42% of the ambition in the Scottish Climate Change Plan Update4.

The UK’s National Grid has produced an annual future energy scenarios to show how the energy system can strive towards Net Zero by 2050

Energy security in 2050

The UK’s National Grid has produced an annual future energy scenarios to show how the energy system can strive towards Net Zero by 2050.

It has a ‘Consumer Transformation Pathway’ (CTP) that assumes high levels of consumer engagement and transformation – essentially a high electrification scenario. It also has a high hydrogen scenario called the ‘System Transformation Pathway’ (STP) that assumes that the consumer experiences little change in their day to day and utilises hydrogen for heating and their vehicles. Comparing the two gives a glance into how the net zero energy system could unfold, and ultimately, what it means for hydrogen and energy security.

Both systems require hydrogen, but the STP requires a 270% increase in hydrogen over the CTP. This is largely driven by the adoption of residential, commercial, and industrial heating, and road transport where electrification can play a more efficient role instead of hydrogen.

It is clear that the less efficiently we use hydrogen, the less realistic it will be to meet our goals, and the more likely we miss our opportunity to become hydrogen exporters and instead become net importers, lose control to reduce emissions and the more we erode British energy security.

Conclusion

Making long-term strategic decisions based on efficiency will support aspirations for energy security and also enable energy export opportunities to Europe. Failing to do so will keep the UK linked to global trade where the best opportunities are for desert countries that do not have western aligned ideals, such as MENA. “Those who cannot learn from history are doomed to repeat it” – we are living that history and at a pivotal moment in making the right decision.

The IEA has shown hydrogen is almost always the cheapest produced domestically even for importer countries like Japan and Germany

Cracking hydrogen from ammonia is wholly inefficient and requires heat source, so that would be fuel self-consumption, or burning fossil fuels. The latter is achievable because there is no current regulation to track emissions past the production gate. This can be worked around if co-located to capture waste heat, but Ricardo has not yet seen any proposals

So if domestic production is cheaper than importing, why doesn’t the UK just do that?

The key issue is around land availability, project development constraints, and domestic opportunities for mass storage. Is the problem seemingly more manageable if left for other countries to make the decisions, or can the UK be the master of its own destiny?

Maggie Adams & Alec Davies are Hydrogen Consultants at Ricardo.

- Energy Security – Topics – IEA

- https://nic.org.uk/studies-reports/national-infrastructure-assessment/second-nia/

- https://royalsociety.org/-/media/policy/projects/large-scale-electricity-storage/Large-scale-electricity-storage-report.pdf

- Press releases | News and insights | Ricardo